http://www.theglobeandmail.com/news/british-columbia/clark-relaxes-student-loan-repayment/article4370350/

Premier Christy Clark says she’ll ease loan payments for students in British Columbia – in some cases forgiving further payments – as the third pillar of her Families First agenda.

-----------

D - but BC charges the HIGHEST interest rate of any province: prime +2.5%.

So thanks for NOTHING.

-----------------

BC: the cowboy wearing the black hat!

--------------

http://m.theglobeandmail.com/news/british-columbia/the-crushing-weight-of-student-debt/article625694/?service=mobile

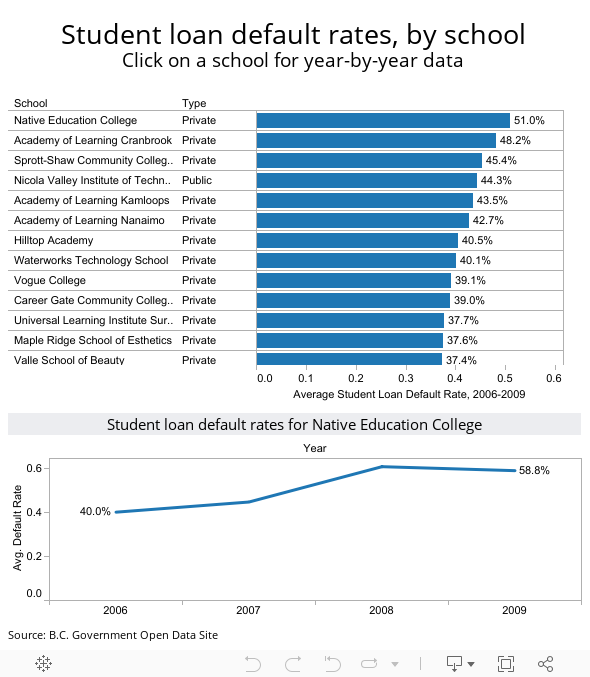

The situation is so critical that, in British Columbia, the heads of four of the province's leading research universities appealed to the provincial government to do something to alleviate the financial stress B.C. students are facing.

B.C. currently charges the highest interest rates on student loans of any jurisdiction in the country - 2.5 per cent above prime. (That compares with Newfoundland, which eliminated interest rates on student loans in 2009.) Worse, B.C. eliminated its student grant program in 2004 and replaced it with a loan-reduction program that forgives millions in debt each year but only for students with certain degrees and who are willing to work in certain areas of the province.

In B.C., interest begins accumulating on a student's debt right after studies are completed. Other provinces have a six-month grace period before this occurs, giving students a chance to establish themselves in a job before their higher loan payments begin. The university bosses would like to see the province adopt a grace period and reduce the interest rate from its current level.

The presidents believe, rightly, that the high cost of financing a postsecondary education is scaring away students from underrepresented groups such as aboriginals and others from impoverished backgrounds. But costs are scaring away kids from middle-class homes as well. And the loans needed to finance those costs are making life miserable for kids trying to get a toehold in a job market that's as unfriendly as they come.

Hope you don't plan to get your PhD on student loans:

---------

Government loans

Canadian citizens, permanent residents of Canada living in any province for over a year, and protected persons

[1] are normally eligible for loans provided by the

federal government, through the CSLP, in addition to loans provided by their province of residence.

Loans issued to full-time students are interest free while a student is in full-time studies. Students receiving a Canada Student Loan (CSL) for the first time on or after August 1, 1995, are eligible for up to 340 weeks (~6.5 years) of interest-free assistance. Students in doctoral programs are eligible for an additional 60 weeks, up to 400 weeks (~7.5 years). Students with permanent disabilities and students who received their first CSL prior to August 1, 1995 are eligible for up to 520 weeks of assistance (10 years).

[2]

As the length of North American graduate degree programs often exceed this 400 week maximum, students considering graduate study are advised to think carefully before taking out student loans. For example, an honours BA from a Canadian University takes four years, assuming satisfactory progress. MA programs in Canada vary in length from 1-3 years, with two years being the average minimum. A PhD, takes on average, 5 years to complete, although many students take significantly longer than this. Assuming a graduate student completes an honours BA (5 years), an MA (2 years), and a PhD (5 years), one can expect to be in university for at least 12 years. This is significantly longer than the 400 weeks maximum allotted to complete a degree by the National student loan program, and

graduate students can easily find themselves in a position where they no longer qualify for student loans. Whether in receipt of student loans or not, students in full-time study are not required to repay their student loans, nor does interest accumulate.

[3] That said, a graduate student who has exceeded the 400 week maximum will be expected to repay their student loan while in school and interest will accumulate on their loan while they are a full time student.

[4]