http://www.statcan.gc.ca/pub/81-004-x/2011001/article/11432-eng.htm

However, parental expectations regarding the financing of their children's postsecondary education do not always match their actual experiences. Shipley (2003) found, for example, that the percentage of children receiving scholarships was far less than the share of parents who expected income from this source. Instead, the percentage of students taking out private loans from financial institutions or from family, friends or a spouse was much higher than parents had expected before their child went on to postsecondary studies.

Similarly, Ouelette (2006)2 found that, generally, no single source of funding was sufficient to cover the basic costs of postsecondary programs for a majority of students.

These (government) programs are designed to ease and increase savings, thereby alleviating some of the financial burden on students during and after graduation.

(D - but are of little use for the abjectly poor family. In fact, in many respects, it merely serves to subsidize the middle class.)

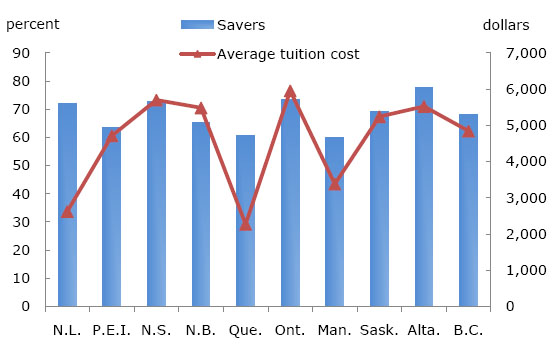

With the exceptions of Newfoundland and Labrador and Quebec, the proportion of savers generally follows the same trend as average tuition fees for Canadian full-time students, suggesting that a strong relationship exists between the cost of postsecondary education and postsecondary education savings patterns across the country.

As shown in Chart 2, the proportion of parents who had saved for their children's postsecondary education increased with income. Not surprisingly, the proportion of savers was highest among the highest income quintile group.

(D - still, about 1/2 that rate still saved in the lowest quintile.)

Previous research has established that a close relationship exists between income and educational attainment. That relationship is reflected in patterns of saving for children's postsecondary education. As shown in Chart 2, parents with less than a high school diploma saved in about the same proportion as those from the lowest income quintile (at 45% and 48%, respectively). At the opposite end, parents with university undergraduate and graduate degrees, at 78% and 80%, respectively, had about the same proportion of savers as those in the highest income quintile (83%).

The balance between saving for retirement and saving for children's postsecondary education can create a juggling act for many parents, with the necessity to ensure their own financial security in retirement, on the one hand, and the desire to give their children the opportunity to pursue a postsecondary education, on the other.

---------------

D - the young GenY parents, who have the highest tuition debts to date,

have their debt, house mortgage, their kids' schooling, then retirement to consider. Brutal. And education will get neglected as Boomers cause a fisal crisis in their old age.

No comments:

Post a Comment